Page Contents

Whereas picture voltaic manufacturing steps are measured in nanometers, atomic layers, and fractions of a share or cent, ingot and wafer manufacturing further rigorously resembles a heavy enterprise. Gleaming crystalline silicon ingots emerge from towering pullers to be sliced by diamond wire saws into iridescent, black sq., or rectangular, monocrystalline wafers.

The ingot and wafering manufacturing steps are power-hungry and produce waste inside the kind of kerf slurry – the residue ingot supplies from between the sliced wafers. These are the PV manufacturing steps most extraordinarily concentrated in China.

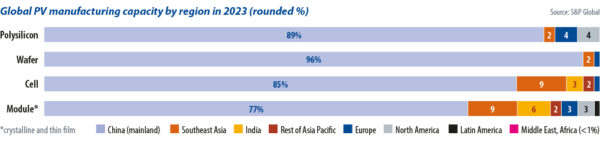

Jessica Jin is the principal evaluation analyst for picture voltaic and clear energy know-how at S&P Worldwide Commodity Insights Shanghai. Jin reported that in 2023, China accounted for 96% of world ingot and wafer manufacturing. She added that the wholesale swap inside PV manufacturing from multi-crystalline to monocrystalline know-how, in and round 2018, was decisive for China’s dominance of the manufacturing step. That dominance has extended upstream.

“This was led by Longi, as all people is conscious of,” she talked about. “Since then, Chinese language language gear producers working with Longi maintain enhancing their know-how and as well as add functionality they normally all develop up with the market enlargement in China.”

The occasion is frequent all by means of China’s picture voltaic success story. By aggressive scaling and shut cooperation with know-how and supplies suppliers, Chinese language language producers have been able to rapidly adapt new know-how and manufacturing processes, outcompeting European and American rivals first on worth, after which on effectivity and effectivity.

“Today, we see most of these gear suppliers are moreover in China as correctly,” talked about Jin. The result’s that in 2024 there are few credible pathways for non-Chinese language language producers excited by rising ingot and wafer functionality.

European setbacks

PV manufacturing advisory Exawatt, now a part of CRU Group, finds that the one notable ingot and wafer manufacturing hub exterior of China is in Southeast Asia. Exawatt tallied some 35 GW of wafer companies in operation in Southeast Asia by the highest of 2023, with that doubtlessly rising to 45 GW by the highest of 2024.

Whereas expansions are underway in South East Asia, the opposite is the case in Europe. The yr 2023 observed every Norsun and Norwegian Crystal droop or wind up their operations in Europe – efficiently reducing wafer manufacturing in Europe to zero. These selections have been adopted shortly after by that of, presumably, a key supplier. Polysilicon producer REC Photograph voltaic Norway began winding up its operations in Kristiansand, Norway – which had an annual output of 8,000 tons – and in Heroya, Norway – with 5,500 tons – in November 2023.

Norwegian Crystal had closed its 500 MW ingot facility in Glomfjord, Norway, a month earlier. As only in the near past as 2022, it had been pursuing plans to develop a 6 GW ingot and wafer facility nevertheless had been unable to save lots of funding, forcing it to start out liquidation of the company.

In September, compatriot Norsun launched layoffs and a producing halt at its 1 GW facility in Årdal, Norway. Tellingly, Norsun is now making an attempt to establish a 5 GW ingot and wafer manufacturing facility within the US. In August 2023, it launched it had raised NOK90 million ($8.5 million) in capital in pursuit of the plan, alongside the €53.6 million ($58 million) it was awarded by the European Union Innovation Fund.

States potential

Subsidies will be discovered for picture voltaic producers in Europe nevertheless they pale as in comparison with what’s on provide within the US. Inside the first 12 months after the US Inflation Low cost Act (IRA) was signed into laws, bulletins have been made totaling 155 GW of annual picture voltaic manufacturing functionality, correct all through the value chain, by commerce physique the Photograph voltaic Vitality Industries Affiliation. Nonetheless, few have been for ingot and wafer manufacturing.

“Consistent with our model, the motivation is superb for manufacturing within the US,” talked about S&P Worldwide’s Jin. “Nonetheless it’s not merely regarding the manufacturing worth however moreover completely different costs, identical to the recycling, improvement worth, and so forth.”

Jin talked about that securing environmental approvals for wafer operations would possibly present the powerful exterior of China. Nonetheless, she did discover that beforehand 5 years, a lot of the waste and recycling factors from wafer manufacturing have been addressed.

South Korean module maker Qcells stands out as an exception. In January 2024, Qcells launched a $2.5 billion funding dedication which included 3.3 GW of annual ingot, wafer, and cell manufacturing functionality, to be executed in ranges. The manufacturing will include the establishment of a model new manufacturing base, in Cartersville, Georgia – the outside of the city of Atlanta within the US. It follows the enlargement of Qcells’ module assembly operations, to 5.1 GW functionality, in Dalton, Georgia, within the US, completed in October 2023.

Present deal

In January 2024, Qcells launched it had expanded the present 2.5 GW module present and engineering, procurement, and improvement suppliers deal with Microsoft to 12 GW of present over eight years. The companies say the duties coated by the deal will be offered by Qcells’ “completely built-in picture voltaic present chain manufacturing facility in Cartersville,” to the tune of 1.5 GW per yr by 2032.

The deal gives offtake certainty to Qcells, with one-third of its ingot and wafer output accounted for in cooperation with a bankable counterparty. For its half, by working with Qcells on this implies, Microsoft hopes to hurry up its renewable energy deployment by locking in and driving large-scale residence manufacturing of picture voltaic modules throughout the course of.

“There could also be always one factor that makes present to the US not sure,” talked about Alex Barrows, head of PV at Exawatt. “I can see an enchantment to locking in a single factor that provides you some certainty – even within the occasion you’re paying a premium.” PV module prices are higher within the US and there stays a complicated web of tariffs, exemptions, border seizures, moratoria, and approved challenges, all of which could delay remaining mission realization or blow out costs.

European producer’s problem ‘plea’

On Jan. 27, 2024, the European Photovoltaic Manufacturing Council (ESMC) issued a “plea for survival” to European policymakers. It argued that abroad PV module producers have been dumping modules, or selling under-price. It moreover pointed to the picks to cease European operations taken by Norsun, REC Photograph voltaic Norway, and Norwegian Crystals – along with the winding up of the German module manufacturing traces of Swiss agency Meyer Burger. “The closure of PV module producers may also be closing potentialities to develop completely different elements of the PV value chain and European supplies and half producers are thus moreover at very extreme menace,” the ESMC talked about in a press launch. “Dropping nearly all European PV module producers correct now would have irreversible unfavorable penalties for the entire EU PV manufacturing enterprise,” talked about the ESMC’s Žygimantas Vaičiūnas. He talked about that emergency measures needs to be launched by the middle of February 2024, “on the most recent.”

Barrows are well-known that Qcells’ father or mom agency, Hanwha, is South Korean considerably than Chinese language language. It has entry to American polysilicon from REC Silicon and is on learn how to change right into a vertically built-in United States producer – making it well-placed to provide stability within the face of potential protection turmoil or geopolitical shocks. “I really feel prefer it’s a reasonably good resolution to lock in some security,” talked about Barrows.

However whatever the IRA, higher prices, and advantages for regionally produced merchandise, Barrows stays skeptical of the prospects of many launched ingot and wafer companies within the US. Alongside Qcells and Norsun; Convalt Vitality, CubicPV, and India’s Vikram Photograph voltaic have launched American manufacturing plans that attain up the supply chain to ingots and wafers.

“I really feel we’ll get a bit [of ingot and wafer capacity] throughout the US nevertheless nowhere near what has been launched,” talked about Barrows. “Thirty-five GW of functionality by the highest of 2026 has been launched nevertheless I might suspect it is further attainable that 15 GW to twenty GW will be put in.”

Kerfless promise

On the guidelines of aspiring producers, CubicPV stands out. Not solely has it launched its intention to develop 10 GW of typical ingot and wafer know-how, nevertheless moreover it is usually a proponent of “direct wafer” utilization. The company’s chief govt officer (CEO), Frank van Mierlo, beforehand led 1366 Utilized Sciences. That enterprise had tried to commercialize “direct wafer” know-how by producing multi-crystalline picture voltaic wafers from a liquid, considerably than cleft from a monocrystalline ingot.

Qcells labored in partnership with 1366 Utilized Sciences and achieved notable conversion effectivity achievements with the latter’s know-how, along with cells with higher than 20% effectivity. Nonetheless, when the PV enterprise switched to monocrystalline know-how, 1366’s wafers had been left stranded on the unsuitable side of development.

Germany’s NexWafe is pursuing a wafer know-how not dissimilar to that utilized by 1366. The NexWafe technique is described as epitaxial and consists of gases being deposited onto a seed substrate from which it could be separated and long-established proper right into a cell. Every strategy will probably be described as “kerfless” wafer manufacturing as they forged off wafer chopping and the waste kerf it produces.

In October 2023, NexWafe broke the ground at a 250 MW manufacturing facility in Germany the place it will make investments of not lower than €70 million. Curiously, NexWafe CEO Davor Sutija was the earlier president and CEO of SiNor, which finally turned Norwegian Crystals.

Manufacturing choices to the mature Czochralski course for monocrystalline ingot pulling and diamond wire sawing ought to overcome capital expenditure, throughput, and effectivity challenges to change into commercially viable. Extreme cell efficiencies on epitaxial or direct wafer know-how have not however been reached, nor has aggressive throughput from a producing facility at scale.

Manufacturing choices to the mature Czochralski course for monocrystalline ingot pulling and diamond wire sawing ought to overcome capital expenditure, throughput, and effectivity challenges to change into commercially viable. Extreme cell efficiencies on epitaxial or direct wafer know-how have not however been reached, nor has aggressive throughput from a producing facility at scale.

The establishment of any new ingot and wafer functionality with any know-how might even occur beneath intense worth opponents. The yr 2023 observed module prices decline by higher than 30% on worldwide markets and there is a glut of merchandise within the market. “We’re anticipating a wash throughout the enterprise subsequent yr,” talked about S&P Worldwide’s Jin.

However, in events of chapter and consolidation, there are options for “step change” or next-generation utilized sciences. European or United States companies would possibly prosper whereas oversupply grips their Chinese language language rivals. NexWafe and CubicPV are pursuing new approaches to wafer manufacturing no matter manufacturing-segment adversity.

In November 2023, NexWafe appointed Rick Schwerdtfeger as chief know-how officer and André Seemaier as chief financial officer because the company strikes into the commercialization a part of its gas-to-wafer know-how.